What it does

Daily Pulse trades one simple, deeply tested idea: when the Nasdaq is in an uptrend and sells off hard over a day or two, it tends to snap back. The strategy buys those dips and exits on the recovery — typically holding 3–4 days, in the market only about 31% of the time.

Entry requires price above the 200-day average (uptrend filter) and RSI(2) signalling a sharp short-term selloff. A second tranche is added at half size if the dip deepens. Exit is the snap-back — a close above the short-term average — or a time stop. Position sizing is risk-based and scales with account equity. Longs only. No martingale, no grid, no hidden logic beyond the protected signal engine.

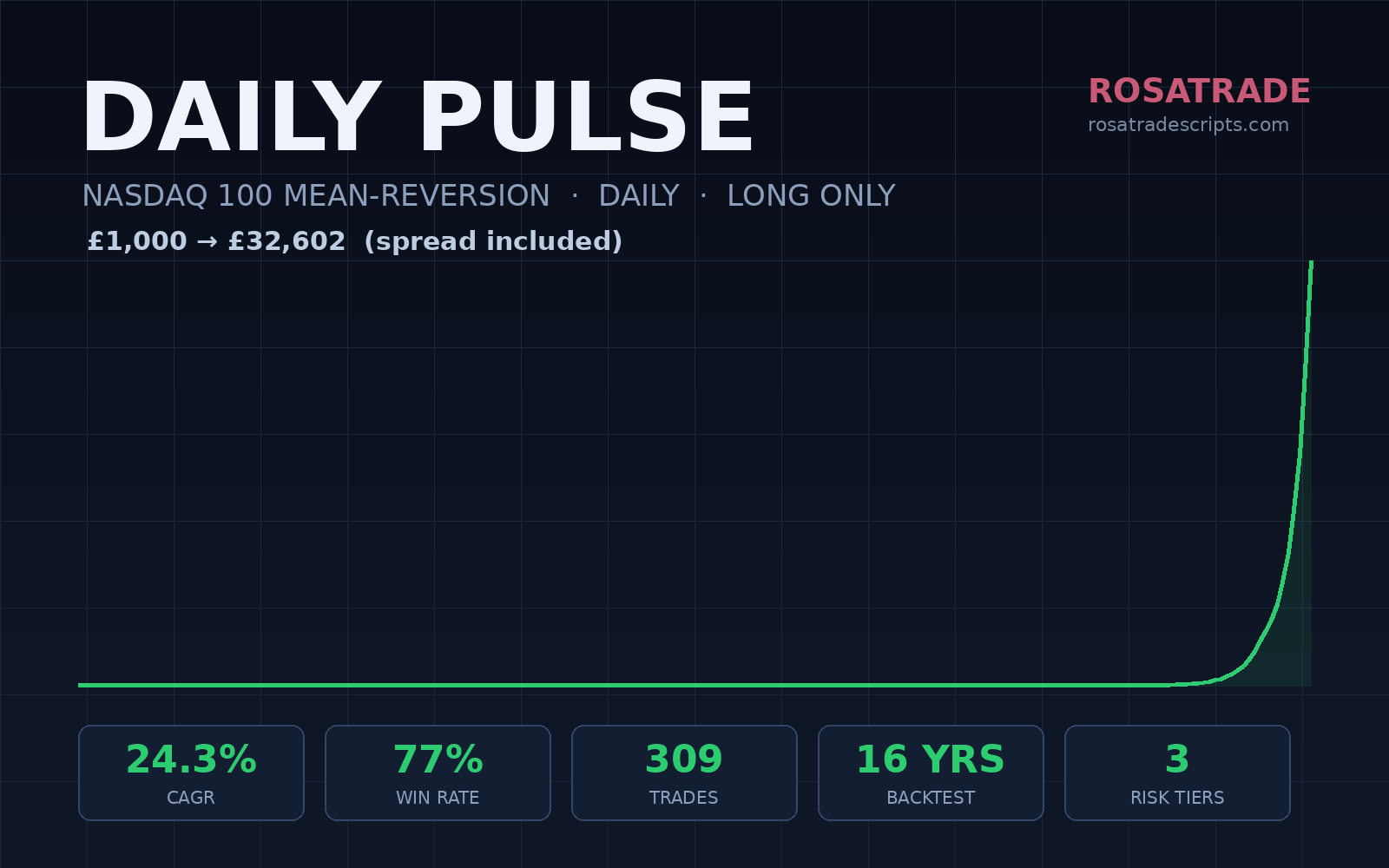

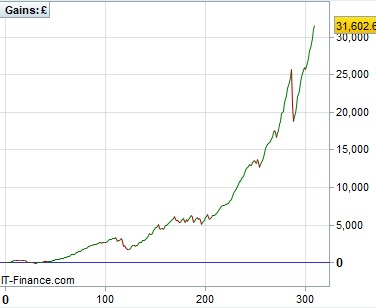

Results (backtest, 1 Aug 2010 – 8 Jul 2026, 3.5pt spread included)

£1,000 → £32,602. CAGR 24.3%, maximum drawdown 26.0%, 309 trades, 77% win rate, gain/loss ratio 2.78, average hold 4 bars.

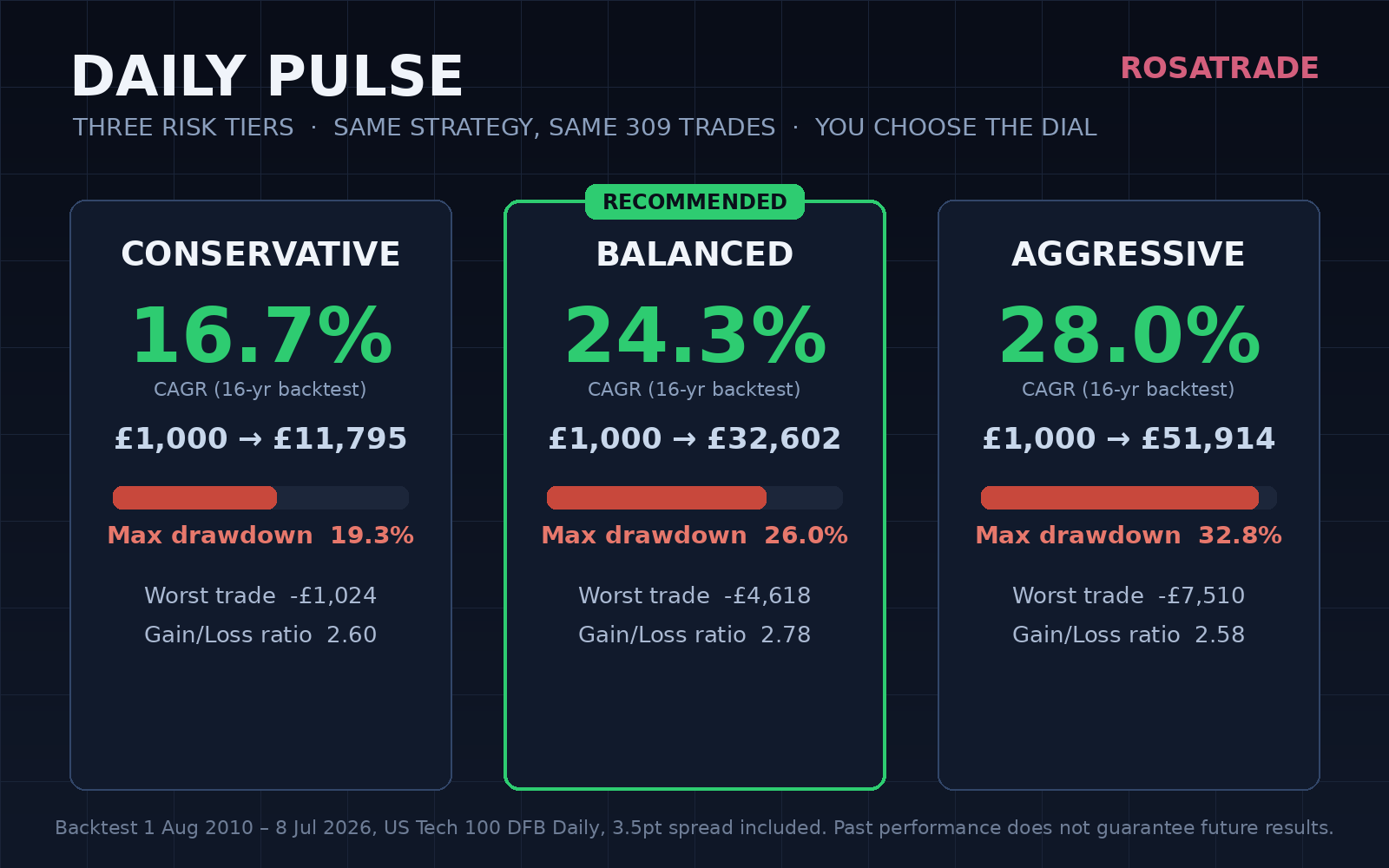

This is the Balanced configuration — the recommended tier of the Daily Pulse family. Two further configurations exist from the same signal engine: Conservative (CAGR 16.7%, max DD 19.3%) and Aggressive (CAGR 28.0%, max DD 32.8%). All three produce the same 309 trades; only the risk sizing differs. The full three-tier edition is available at rosatradescripts.com.

Honest disclosure — read before buying

The drawdown figure above is real and includes the early-2026 correction. It is structural to this edge: the strategy buys falling markets, and occasionally a dip becomes a crash before the exit triggers. During development, seven different protective mechanisms (stops, entry filters, velocity gates, time-stop variants) were tested to reduce the maximum drawdown. All seven were rejected because each destroyed more profit than drawdown — the losing trades are not separable from the winning ones at entry. Risk sizing trades return for drawdown; nothing removes the risk.

This is a long-only strategy on a single instrument. It will have losing months and flat periods. Expected frequency is roughly 20 trades per year. Win rate is high but average losses are larger than average wins — that is the character of mean reversion. Past performance does not guarantee future results.

What you get

The Daily Pulse strategy for ProRealTime ProOrder (protected code, single-file import — the signal engine is included inside), setup instructions for IG US Tech 100 DFB on the Daily timeframe, and the position-sizing explanation. Questions answered via marketplace messaging.

Requirements: ProRealTime with ProOrder (IG). Designed and tested on US Tech 100 DFB, Daily timeframe, CFD/spread-betting. Not tested on futures or other instruments.

Recensioni

Ancora non ci sono recensioni.