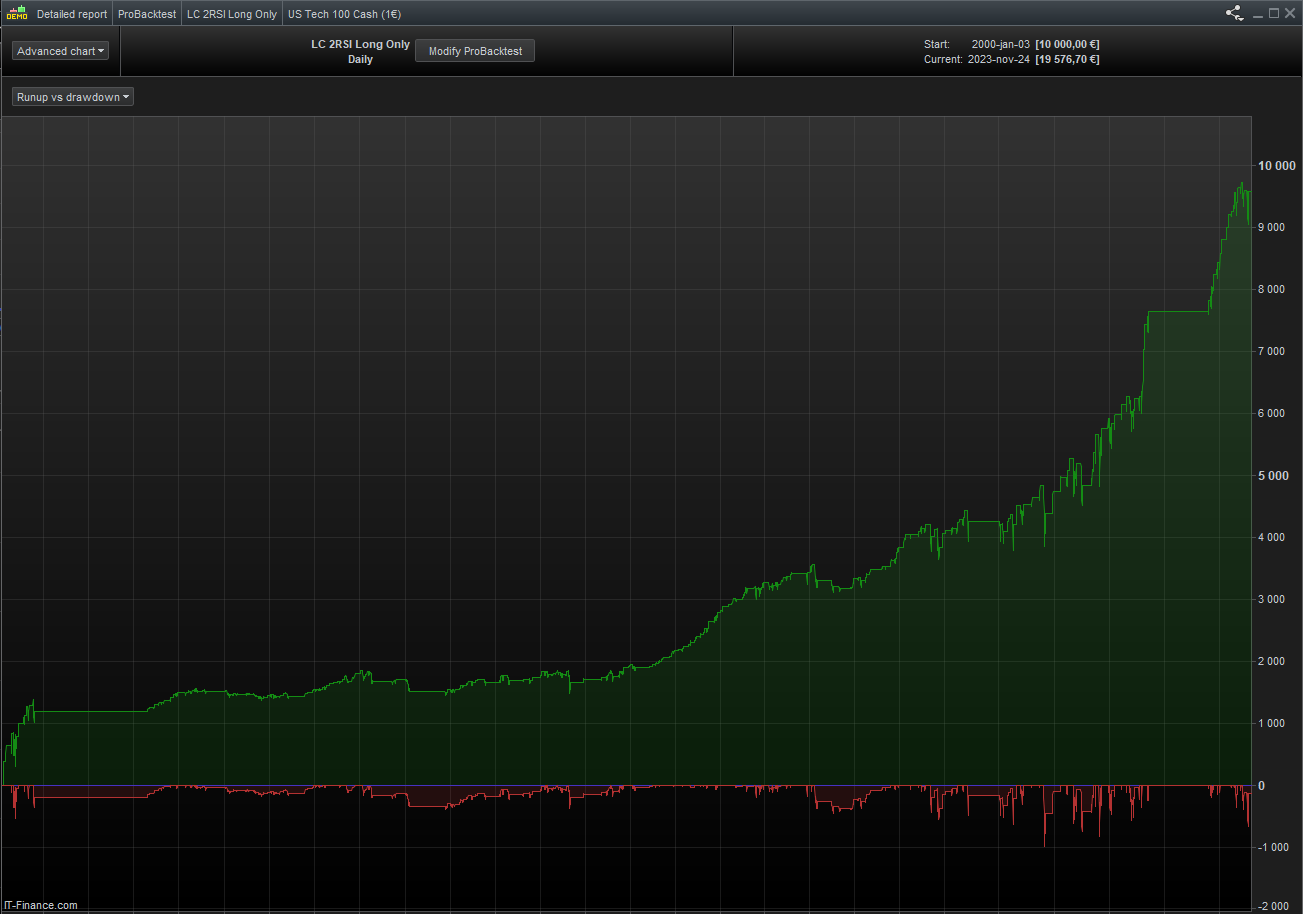

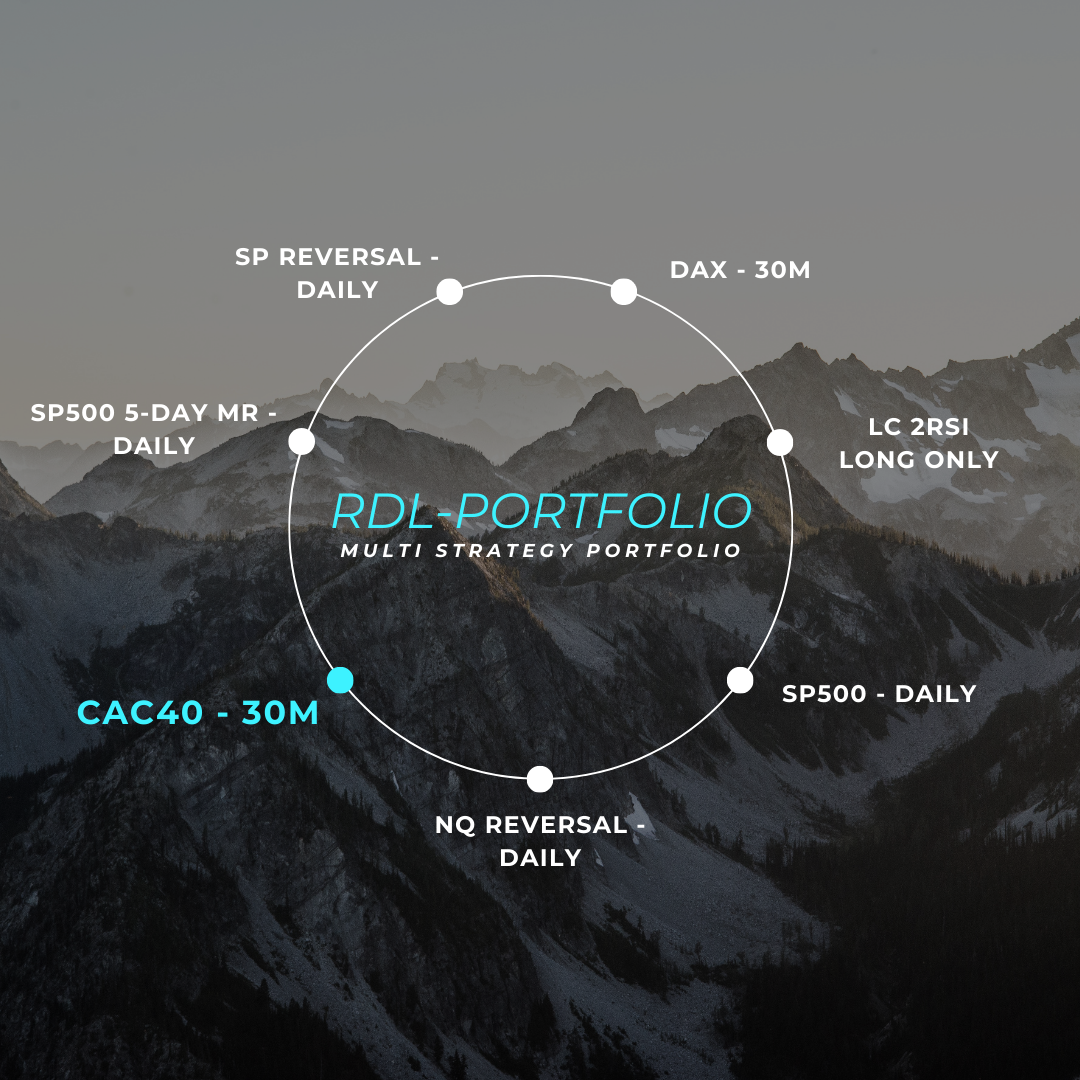

This strategy is very simple and built with only a MA Crossover and a RSI filter. The Simplicity in the code makes this strategy extremely robust and profitable. It works on multiple timeframes and instruments but for our RDL-Portfolio Bundle we have chosen to go with the NQ Daily setting.

Check out the historical results for the RDL-Portfolio here: https://www.algomatictrading.com/performance

Reviews

There are no reviews yet.